The majority of complaints finalised by the Pension Funds Adjudicator in its financial year to the end of March were from people who had not yet received or had only partially received their retirement savings on leaving their pension fund.

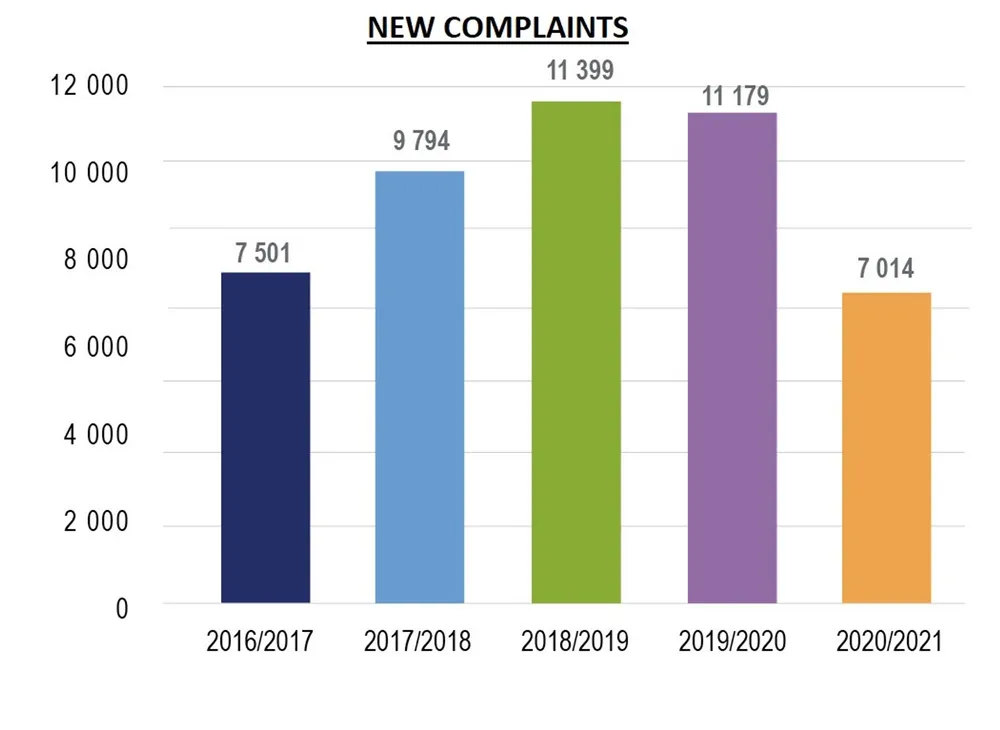

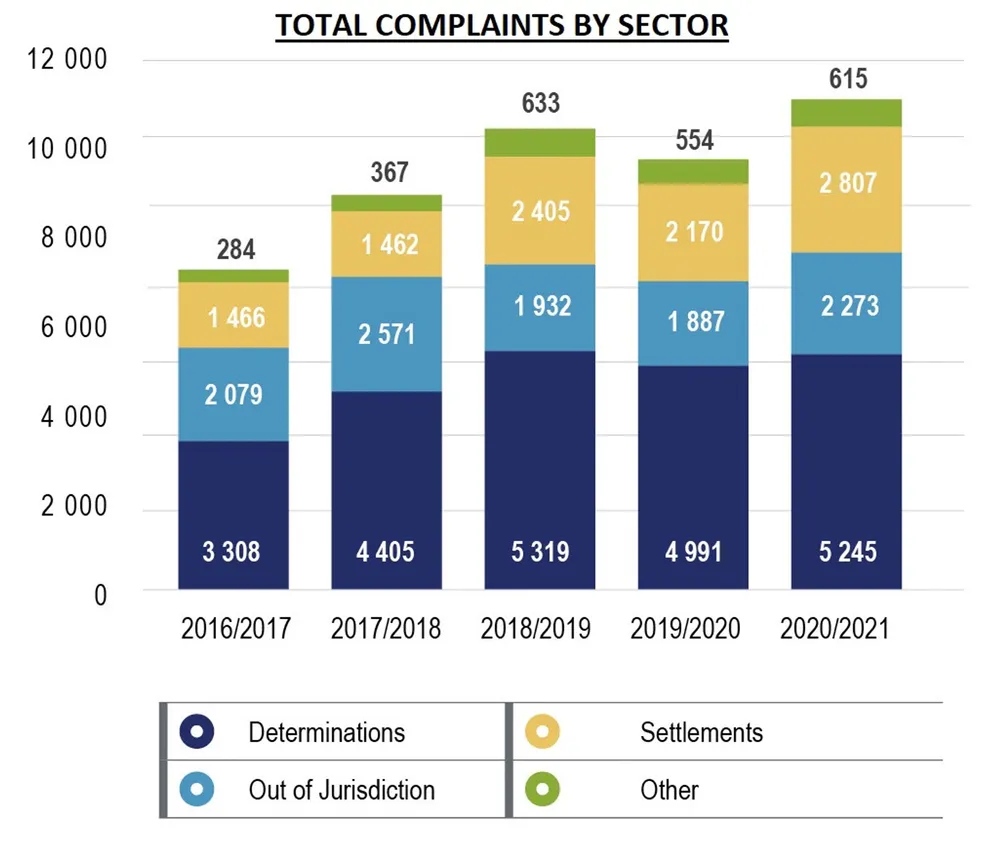

In its annual report released this week, the office of the adjudicator reveals that of the 10 940 complaints finalised in the 2020/21 financial year, 52.9% related to retirement fund withdrawal benefits.

The delayed payment or non-payment of retirement benefits may be because of slack administration practices by the fund administrator, the documentation on a member being incomplete or out of date, or, more concerningly, because the member’s employer failed to pay over contributions to the fund or even failed to register the member with the fund in the first place, while deducting the contributions from the member’s salary.

Complaints relating to the non-payment of retirement fund contributions by employers (non-compliance with section 13A of the Pension Funds Act) came second, at 23.9%, according to the annual report.

Another area of complaints that appears to take up much of the time of Pension Funds Adjudicator Muvhango Lukhaimane and her staff is the distribution of death benefits. As detailed in last week’s article, “The payment of retirement benefits on death – it’s complicated”, fund trustees often have an onerous task in deciding to whom these benefits should be distributed, and disputes often arise. Almost 7% of complaints finalised related to the payment of death benefits, as governed by section 37C of the Act.

Lukhaimane said clarity continues to be provided to funds by her office, the Financial Services Tribunal, the various High Courts and the Supreme Court of Appeal on the interpretation of section 37C.

“It is most prudent that funds and administrators invest in training initiatives within their boards of management or organisations to ensure that technical expertise or knowledge on how to deal with death benefit payments is shared and maintained. The lack thereof is apparently clear from the issues that get misinterpreted, as these are often not complex at all nor do they raise novel issues,” Lukhaimane said.

Biggest offender

The Private Security Sector Provident Fund (PSSPF) remains the biggest source of complaints, according to the report. This fund serves the employees of the innumerable private security firms around the country, and has long been a cause for concern among the regulators.

The Financial Sector Conduct Authority (FSCA) conducted a supervisory on-site inspection of the PSSPF in November 2017. Following its findings, the FSCA applied for the appointment of curators to take control of the business of the PSSPF and, with theagreement of the fund, appointed statutory managers to the board of the fund in September 2018. The statutory managers commissioned an independent forensic investigation on the PSSPF, while the FSCA conducted an investigation into the affairs of the PSSPF and the appointment of SALT Employee Benefits as a service provider to the fund. Following the findings emanating from these interventions, the FSCA proceeded with regulatory action against various parties.

“This regulatory action is an on-going and confidential process, in terms of section 251 of the Financial Sector Regulation Act, and while the FSCA cannot disclose any further details about its findings, it can assure the public that the matter is receiving due attention,” the FSCA said in a recent release.

The adjudicator’s annual report says that, “under statutory management and having increased its complaints management capacity (both in terms of systems and case administrators), the PSSPF’s turnaround times have somewhat improved.

“The only outstanding concern remained the quality of responses that notably required follow-ups and the fact that the fund had failed to take advantage of the revised complaints’ management process as there was no attempt at all on its part to resolve complaints directly with members.”

Treating Customers Fairly

In the report, Lukhaimane said she had ongoing concerns that financial services providers were failing to abide by the Treating Customers Fairly (TCF) outcomes.

Regulated services providers are expected to deliver the following six TCF outcomes to their customers throughout the product life cycle, from product design and promotion, through advice and servicing, to complaints and claims handling:

1. Customers can be confident they are dealing with firms where TCF is central to the corporate culture.

2. Products and services marketed and sold in the retail market are designed to meet the needs of identified customer groups and are targeted accordingly.

3. Customers are provided with clear information and kept appropriately informed before, during and after point of sale.

4. Where advice is given, it is suitable and takes account of customer circumstance.

5. Products perform as firms have led customers to expect, and service is of an acceptable standard and as they have been led to expect

6. Customers do not face unreasonable post-sale barriers imposed by firms to change products, switch providers, submit a claim or make a complaint.

“All in all, [the failure to deliver] the top four outcomes represents 97.3% of all complaints. It can, therefore, be safely concluded that funds, administrators and employers need to put measures in place to improve on TCF outcomes and they must be held accountable for this in order to improve the member experience,” Lukhaimane said.

PERSONAL FINANCE