(AP Photo/Richard Drew)

Words on Wealth

Looking up the performance figures of a unit trust fund may seem simple enough. But to get a true idea of the growth of your investment, you need to know what figures you are looking at and how they have been calculated ‒ and this is where things get a bit complicated.

The fund’s unit price is known as its NAV (net asset value), and it is calculated once a day. The formula is: assets minus liabilities, divided by the number of units. The fund’s assets are the values of its underlying investments; its liabilities are the costs it has incurred, which are the fund’s management costs and other operating expenses. The NAV is the price at which you buy units and at which you sell units.

Note that although the fund’s expenses are factored into the NAV (these are expressed separately as the fund’s total expense ratio, or TER), you may be liable for other costs, such as an additional layer of administration costs of the investment platform on which the fund may lie and advice costs, which will eat into the NAV return.

Following a unit trust fund’s NAV gives you a rough picture of how the fund is performing, but it doesn’t give you the whole picture. This is because the NAV does not factor in what the fund earns on its underlying investments through dividends and interest.

Share investments pay out dividends, and interest-bearing investments, such as bonds and money market instruments, pay out interest. These payments to investors, or income distributions, may occur quarterly or once or twice a year. Depending on whether you are investing for income or for growth, you will either be paid out the distribution amount or it will be reinvested for you in the form of additional units. The NAV will drop directly after a distribution in proportion to the value of the distribution.

This means that if you are reinvesting the income from your investment, which contributes to its compound growth over time, you need to take account not only of the NAV but of the additional units you have accumulated through income distributions in order to accurately assess your growth on that investment.

This more accurate picture of your return is known as your total return, which is the return with dividends and interest reinvested.

The Investopedia website (from which most of this information is sourced), gives the following example for a share investment, which is similar in this respect to a unit trust fund:

An investor buys 100 shares of Stock A at R20 a share for an initial value of R2 000. Stock A pays a 5% dividend, which the investor reinvests, buying five additional shares. After a year, the share price (the NAV in the case of a unit trust) has risen to $22.

To calculate the investment's total return, the investor divides the total investment gains (105 shares x R22 per share = R2 310 current value - R2 000 initial value = R310 total gains) by the initial value of the investment (R2 000) and multiplies by 100 to convert to a percentage (R310 / R2 000 x 100 = 15.5%). The investor's total return is 15.5%, although the share price has risen only 10%.

The extent to which total-return performance exceeds NAV performance depends on the nature of the fund and its assets: some funds derive almost all their returns from the capital growth of the underlying assets while others derive a substantial portion from dividends and/or interest.

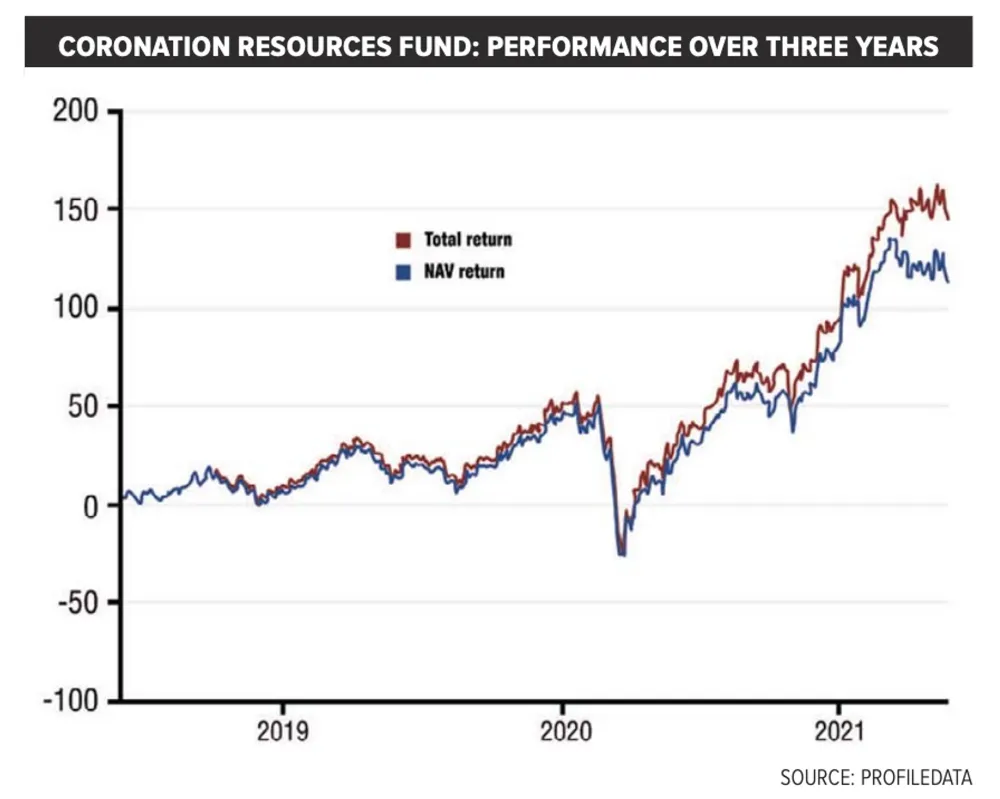

If you are investing for growth, make sure the performance figures you consult reflect total returns. In the graph of the three-year performance of the Coronation Resources Fund, courtesy of ProfileData, there is a clear difference between NAV and total return.

Annualised return

Performance figures typically give a fund’s performance over different periods ‒ say, one, three and five years. The figures for any periods longer than one year are annualised returns ‒ that is, what the fund averaged per year over the period. However, the average is not a simple arithmetic one; it is what is known as a geometric average, and the calculation is more complicated.

Say a fund, over five years, gives you successive annual returns of 3%, 16%, 1%, 2%, and 13%. Taking an arithmetic average, you would say that the fund returned 7% a year over the five years. However, the annualised figure is slightly lower: 6.83%

This can be demonstrated in another way: if you invested R100, a consistent 7% a year would give you R140.26 after five years; the actual sequence of returns results in a lower figure of R139.09.

Averages, be they arithmetic or geometric, have a nasty habit of masking volatility, as shown in this example. When choosing a unit trust investment, you need to dig deeper than its annualised performance figures.

PERSONAL FINANCE